All Categories

Featured

Table of Contents

That typically makes them a much more cost effective option for life insurance coverage. Some term policies may not maintain the costs and survivor benefit the very same with time. Term life insurance for spouse. You do not wish to incorrectly think you're buying level term insurance coverage and afterwards have your survivor benefit adjustment later. Many individuals get life insurance policy coverage to help financially protect their enjoyed ones in instance of their unexpected death.

Or you may have the option to convert your existing term coverage into a permanent plan that lasts the rest of your life. Numerous life insurance coverage plans have prospective benefits and disadvantages, so it's important to understand each before you decide to purchase a plan.

As long as you pay the premium, your beneficiaries will obtain the survivor benefit if you die while covered. That claimed, it is essential to keep in mind that many policies are contestable for two years which implies coverage might be retracted on fatality, ought to a misstatement be located in the app. Plans that are not contestable commonly have a rated survivor benefit.

What is Term Life Insurance With Accidental Death Benefit? Learn the Basics?

Premiums are normally reduced than whole life plans. You're not locked right into an agreement for the remainder of your life.

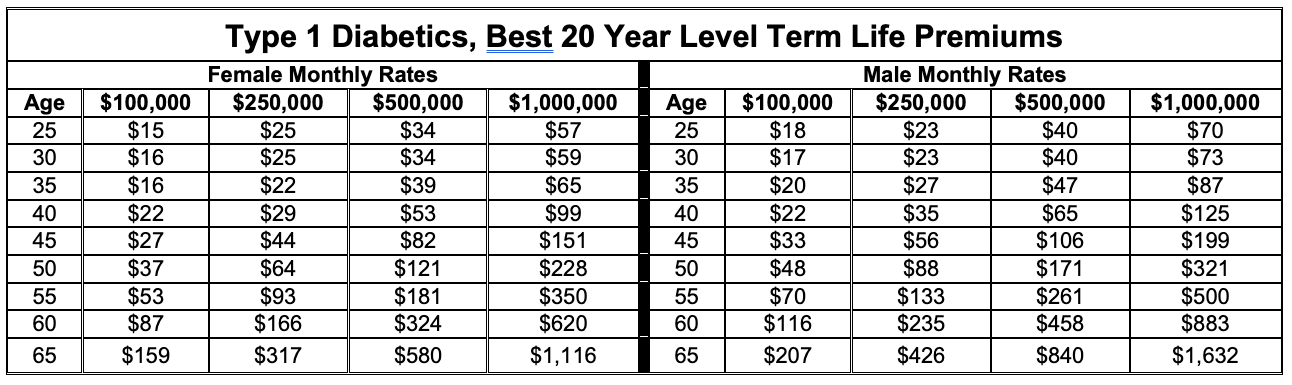

And you can not squander your plan during its term, so you will not obtain any kind of monetary benefit from your past coverage. Similar to other kinds of life insurance policy, the cost of a level term policy depends on your age, insurance coverage requirements, employment, lifestyle and health. Typically, you'll find much more budget-friendly insurance coverage if you're more youthful, healthier and much less dangerous to insure.

Given that degree term costs remain the same for the period of coverage, you'll know specifically how much you'll pay each time. Level term insurance coverage additionally has some adaptability, permitting you to customize your policy with additional functions.

How Does Life Insurance Level Term Benefit Families?

You may need to fulfill particular problems and certifications for your insurance company to establish this cyclist. Additionally, there might be a waiting period of approximately 6 months before working. There likewise could be an age or time frame on the insurance coverage. You can include a child motorcyclist to your life insurance policy plan so it additionally covers your children.

The survivor benefit is typically smaller, and insurance coverage typically lasts till your kid transforms 18 or 25. This rider may be a more cost-effective method to aid ensure your kids are covered as riders can often cover numerous dependents at once. As soon as your child ages out of this insurance coverage, it may be possible to transform the rider right into a brand-new policy.

The most common kind of permanent life insurance is whole life insurance coverage, but it has some key distinctions contrasted to degree term protection. Right here's a standard overview of what to consider when comparing term vs.

What is Term Life Insurance Level Term? Quick Overview

Whole life insurance lasts for life, while term coverage lasts protection a specific period. The costs for term life insurance are generally reduced than entire life insurance coverage.

One of the highlights of level term coverage is that your premiums and your fatality advantage do not alter. With decreasing term life insurance, your costs stay the same; however, the survivor benefit amount gets smaller sized gradually. You might have coverage that begins with a death benefit of $10,000, which could cover a home loan, and after that each year, the death advantage will certainly decrease by a set amount or percentage.

Due to this, it's frequently an extra economical type of level term insurance coverage., yet it may not be sufficient life insurance for your needs.

What Are the Terms in Level Premium Term Life Insurance Policies?

After picking a plan, finish the application. For the underwriting procedure, you may have to supply general individual, wellness, way of living and work details. Your insurer will certainly determine if you are insurable and the threat you may provide to them, which is shown in your premium prices. If you're authorized, authorize the documentation and pay your initial premium.

Finally, think about organizing time each year to evaluate your plan. You may desire to update your beneficiary info if you have actually had any kind of substantial life adjustments, such as a marital relationship, birth or separation. Life insurance policy can occasionally feel complex. But you don't need to go it alone. As you explore your options, think about reviewing your demands, wants and interests in an economic specialist.

No, level term life insurance policy does not have money value. Some life insurance plans have an investment function that enables you to construct money worth gradually. A section of your premium repayments is established apart and can gain rate of interest with time, which grows tax-deferred during the life of your insurance coverage.

You have some options if you still want some life insurance policy coverage. You can: If you're 65 and your protection has run out, for example, you may want to get a brand-new 10-year level term life insurance coverage policy.

What is Term Life Insurance For Couples? Explained in Detail

You may have the ability to transform your term coverage right into a whole life policy that will last for the remainder of your life. Lots of types of degree term plans are convertible. That indicates, at the end of your insurance coverage, you can transform some or every one of your policy to entire life coverage.

A degree premium term life insurance strategy lets you stick to your budget plan while you aid safeguard your household. ___ Aon Insurance Policy Services is the brand name for the broker agent and program administration operations of Fondness Insurance coverage Providers, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Affinity Insurance Policy Company, Inc. (CA 0795465); in Alright, AIS Affinity Insurance Providers Inc.; in CA, Aon Fondness Insurance Coverage Solutions, Inc .

{kind=link}

Latest Posts

Seniors Final Expenses Insurance

What Is The Difference Between Life And Burial Insurance

Aarp Final Expense Plans